Andrew Melville

Research Analyst

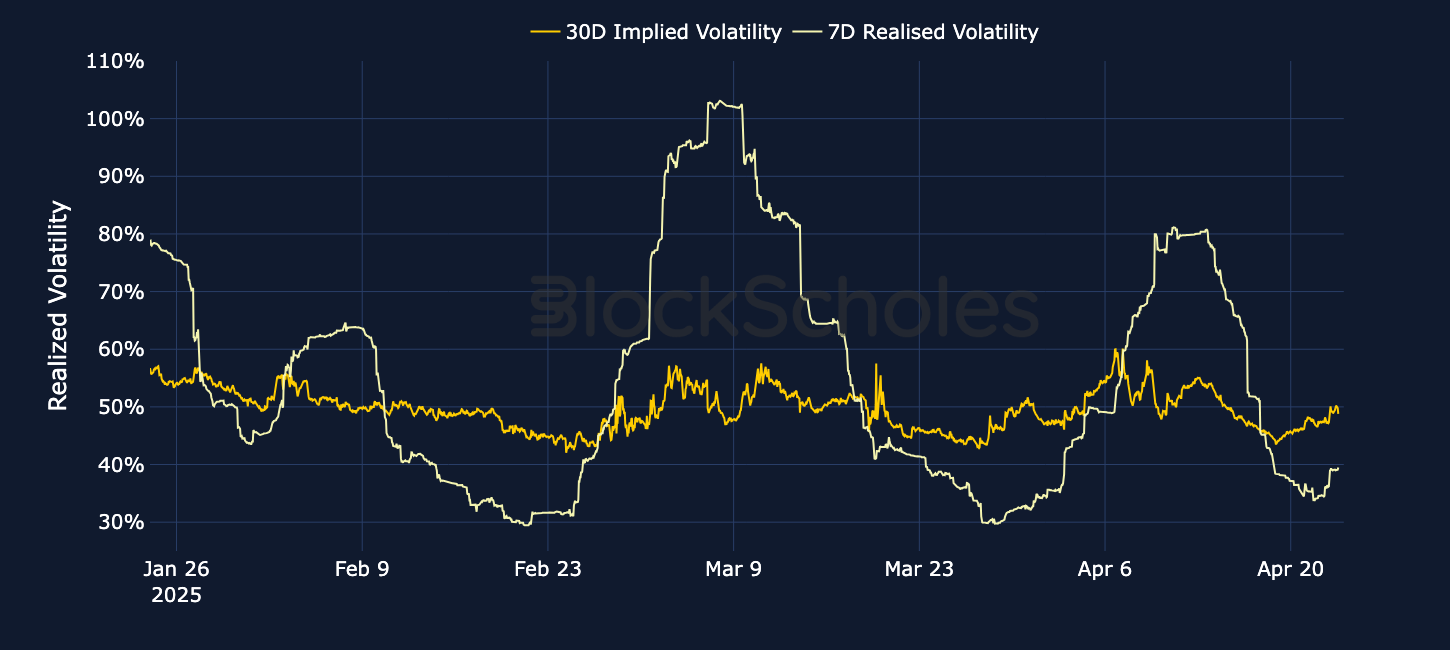

At the start of the week, Bitcoin began to show signs of decoupling from its relationship with US equities. However, following US president Donald Trump's positive comments regarding the US’s ongoing trade war with China (which saw tariffs of 145% imposed on Chinese goods entering the US), a relief rally has gripped markets across asset classes. In turn, BTC has once more been moving up alongside US equities. With that spot move, implied volatility at 7-day and 14-day tenors has jumped, and BTC’s put-call skew has recovered at short tenors, a sign that traders are indeed looking for upside exposure to the rally.

At the start of the week, Bitcoin began to show signs of decoupling from its relationship with US equities. However, following US president Donald Trump's positive comments regarding the US’s ongoing trade war with China (which saw tariffs of 145% imposed on Chinese goods entering the US), a relief rally has gripped markets across asset classes. In turn, BTC has once more been moving up alongside US equities. With that spot move, implied volatility at 7-day and 14-day tenors has jumped by 12 points, and BTC’s put-call skew has recovered at short tenors by more than 5%, a sign that traders are indeed looking for upside exposure to the rally.

Perpetuals: BTC funding rates have remained positive, whereas funding rates for ETH have continued to fluctuate between positive and negative, despite a 12% rally in spot this week.

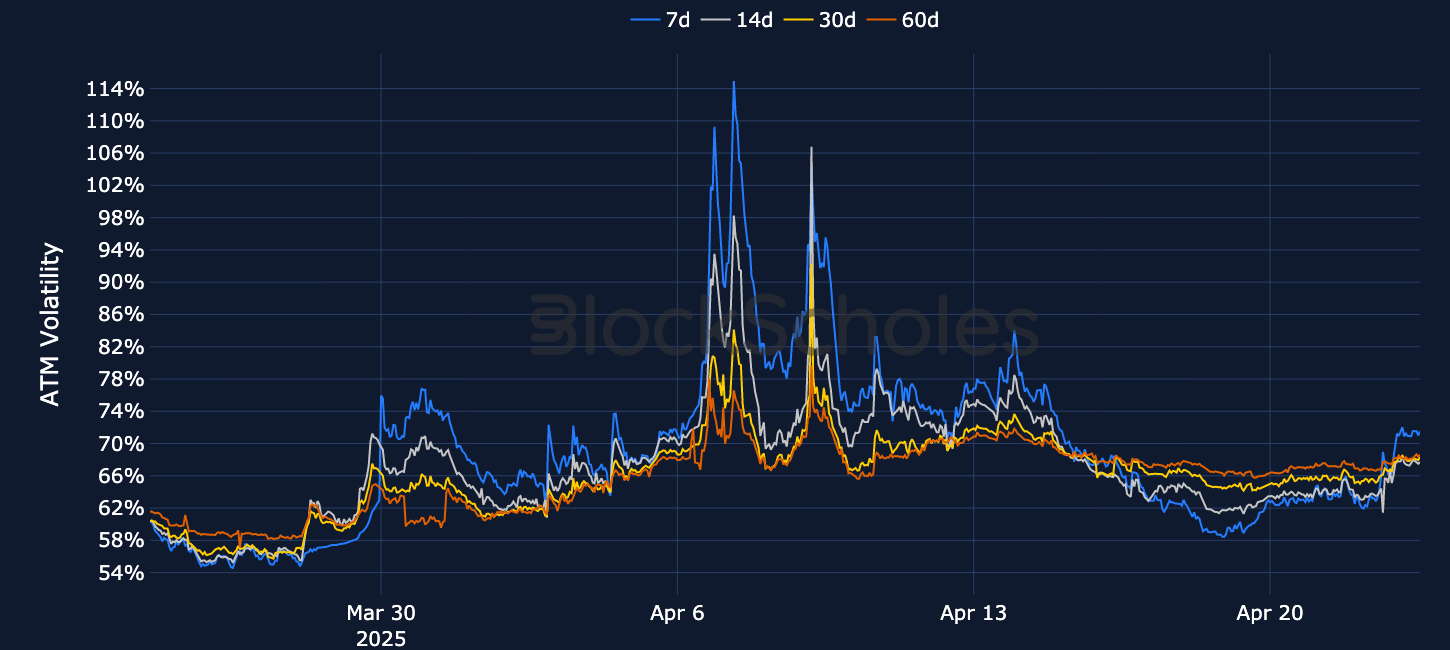

Options: BTC’s term structure has flattened as volatility at the front end picked up from historically low levels, while ETH’s term structure has once again inverted from its brief flat shape.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

Weaker US dollar, stronger Bitcoin — Since President Trump announced (and subsequently) paused his “Liberation Day” tariffs on Apr 2, 2025, BTC’s price has increased by 9%. Meanwhile, the DXY, a measure of the US dollar against a basket of the world’s major currencies, is down by 4%.

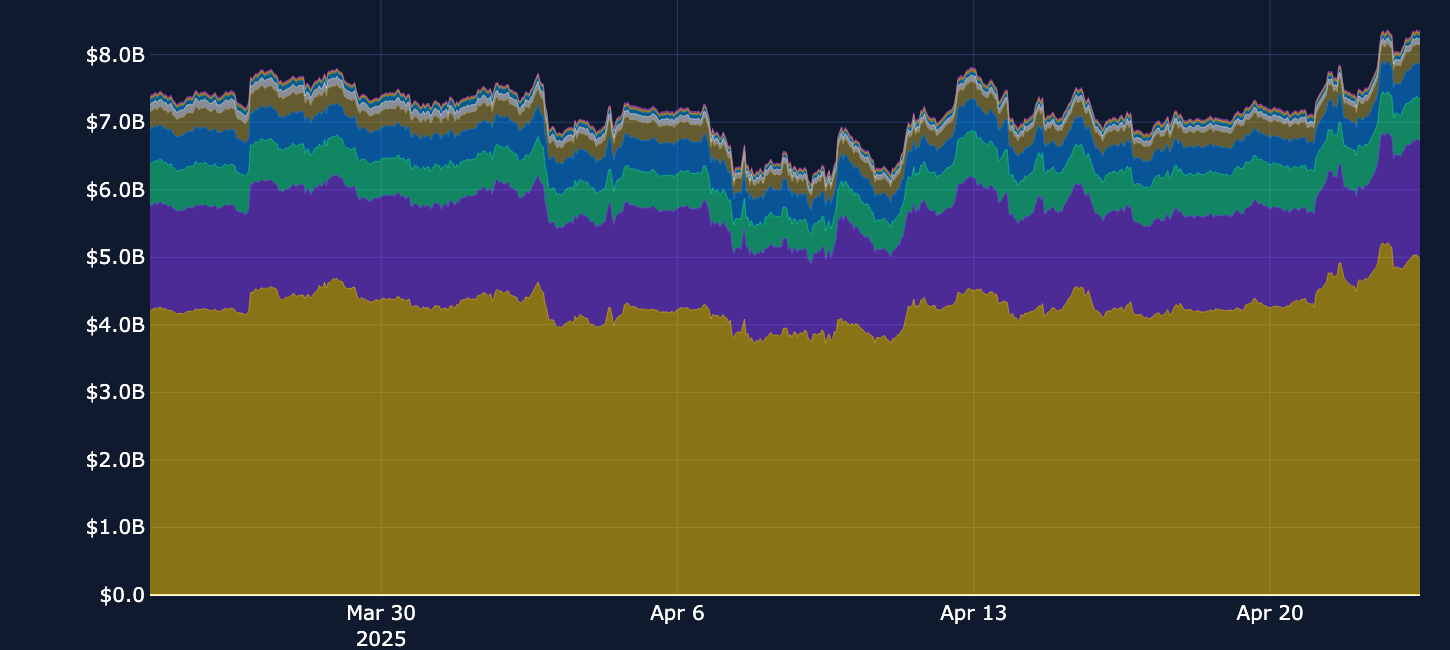

President Trump set off a rally across risk-on US equities by stating that tariffs on China will “come down substantially,” quelling fears that he may attempt to dismiss Federal Reserve Chair Jerome Powell. Bitcoin, which had been rallying even before these comments, subsequently began to move up alongside US equities. In addition, perp open interest has increased noticeably (by 20%) since the beginning of the week across a broad range of tokens, particularly ETH. Perp trading volumes also increased (hitting a high close to $18B), though not to levels seen during the spot price sell off of Apr 7th, 2025. That date saw the highest total trade volume for the month, as President Trump told reporters “forget markets for a second, we have all the advantages.”

Despite the crypto rally being broad-based across a variety of tokens towards the end of the period, funding rates earlier in the week had shown a more mixed picture. Funding rates for BTC, XRP, DOGE, TON and ADA are now positive and rising, a sign that traders are willing to back the relief rally — at least in the short term. However, despite ETH spot price rallying 12% this week and other measures of sentiment (such as the put-call skew) showing evidence of bullish positioning, perp markets aren’t sharing that sentiment. Funding rates for SOL have more recently ticked up following a sustained period of negative rates over the past week. Funding rates for SOL have more recently ticked up following a sustained period of negative rates over the week.

President Trump’s most recent signaling of a willingness to negotiate a trade deal with China’s President Xi has set off a relief rally across asset classes, including crypto. BTC, however, had been rallying this week even before Trump’s comments, with its spot price up 7% since Apr 21, 2025. Despite the rally, open interest in puts has been stronger than in calls, and options volume has been relatively balanced.

It’s not clear whether the demand for puts is a sign that traders are protecting themselves against downside moves, or directionally fading the move upward. Additionally, funding rates in perps don’t tell us too much in terms of sentiment, either. However, the put-call skew, another measure of market sentiment, has recovered by more than 5 points at short tenors — a sign that traders are indeed looking for upside exposure to the rally — and willing to pay for it, too.

ETH’s response to the latest crypto market recovery rally has been a divergence from what we’ve typically seen in this cycle. Not only has ETH outperformed BTC in spot — something it has often failed to do so in recent rallies — but open interest in calls is also higher than in puts, the opposite of what we’re seeing with BTC. In addition, ETH open interest for calls is nearly twice that of puts, and calls have dominated options volumes, too. This could suggest that traders are expecting ETH will pare back some of its relatively large and persistent underperformance again — not just BTC, but other so-called “ETH killers” (such as SUI and SOL). The spot rally has also resulted in another term structure inversion for ETH.

Though Solana is up 20% so far this week, it remains considerably below its January all-time high of $293. Open interest in Solana options remains dominated by calls — as it has been for the past month of rocky spot moves. This open interest is also particularly rooted in later expirations. However, there’s been a significant rise in open interest for puts during the recovery rally (from below $2B to nearly $3.8B), echoing the behavior of BTC options markets to some extent. In comparison to last week, options volumes are once again dominated by calls. Unlike ETH or BTC, SOL’s term structure remains positively sloped, with a significant premium attached to its volatility — as expected for an altcoin like SOL.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)

.jpg)