Andrew Melville

Research Analyst

Since recovering from the selloff in the first week of August, spot prices have largely moved sideways. This period of relative calmness has opened up a space for a divergence in sentiment between BTC and ETH, with metrics across derivatives markets indicating a stronger bearishness assigned to the latter in the short term. ETH futures-implied yields trade significantly lower, perpetual swap funding rates have moved intermittently negative, and options on ETH trade with a premium to BTC’s implied volatility across the term structure, with short-tenor OTM puts afforded an implied volatility premium over OTM calls.

.jpg)

BTC’s curve has flattened over the last 24H, but remains in the same 9-11% rangeThe curve has steepened slightly as front end yields fall while remaining steady for longer tenors.

ETH yields trade lower than BTC’s for each tenor, with short-dated expiries underperforming the most.

A short period of positive funding rates has returned to neutral, indicating low demand to pay for leveraged long exposure.

Has continued to trade intermittently negative over the past two weeks.

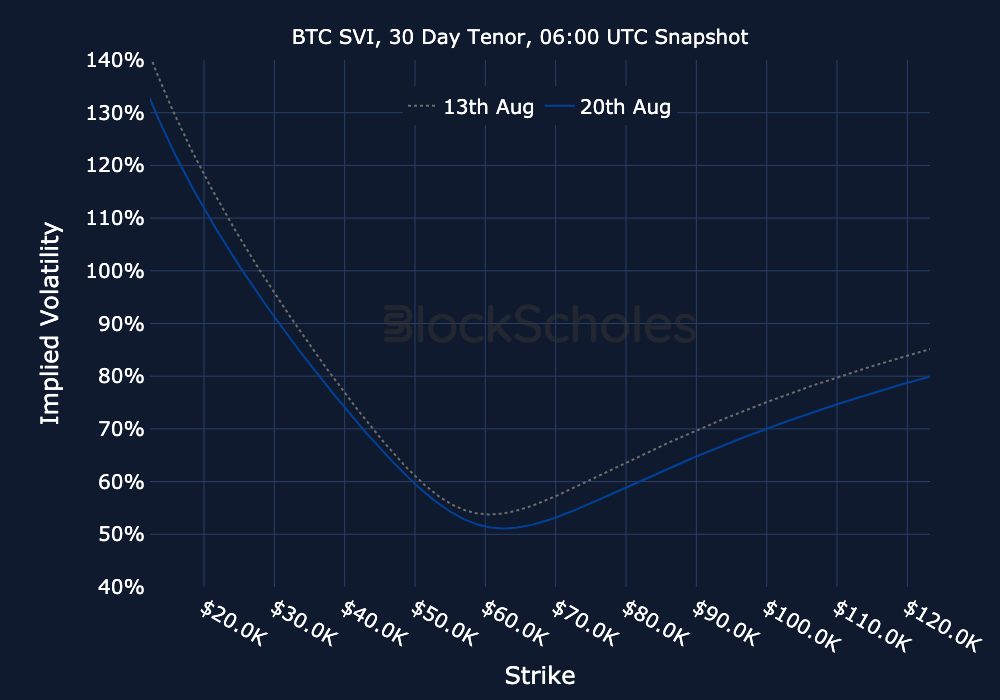

Short-dated volatility has fallen to around 50%, while longer tenor optionality has remained near to 60%.

We still see a divergence in skew between put-skewed short-tenor smiles and call-skewed longer-tenor smiles.

Shows the same steepening in the term structure as BTC but with a premium of 10 points or greater at all tenors.

ETH short-tenor smiles remain more strongly put-skewed than BTC’s and we see the same skew towards calls at a 90D tenor.

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)