Andrew Melville

Research Analyst

One of the largest global market selloffs since the COVID pandemic took its toll on crypto-spot prices, resulting in double-digit selloffs that were harder felt by ETH and alts than BTC. The selloff saw funding rates spike negative as accumualted long positions were likely liquidated, and the volatility term structure inverted as traders rushed to cover exposure to further downside moves in the short term. However, volatility levels did not spike above their year-to-date highs for either major, and longer-dated volatility smiles remained steadfastly skewed towards OTM calls. This indicates that while this was strong move in the short term, traders are not yet concerned about long-term performance.

.jpg)

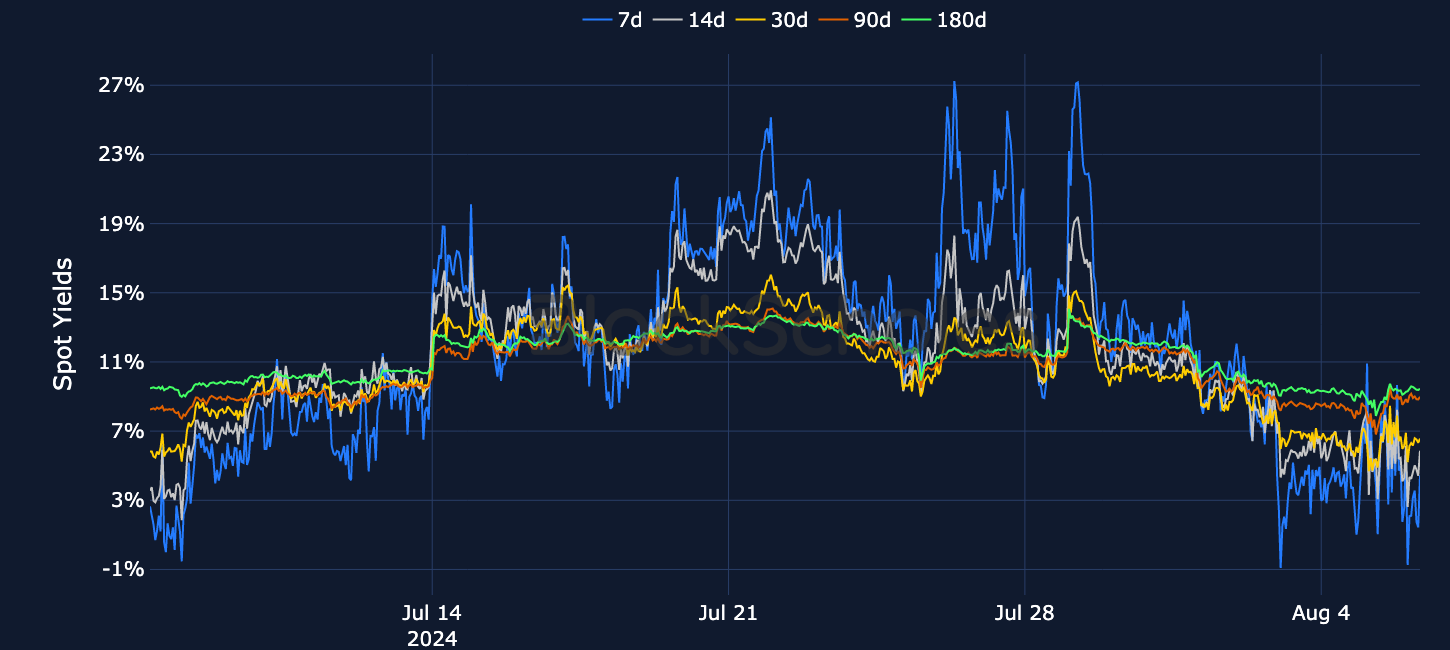

Yields have fallen from their highest levels in months to barely positive in the recent spot sell off

Trade slightly lower than BTC’s at all tenors with the same steep shape of the term structure

Have traded intermittently negative as traders exit long positions and cover short exposure

Spiked far more negative than BTC’s, suggesting a possible liquidation event during the selloff

Volatility levels inverted strongly during the selloff, and have since trailed off

Short tenor options skewed strongly towards puts, but longer-tenor smiles remained steadfastly call-skewed

Shows a similar premium at short tenors to BTC, but trades 10-15 points higher across the term structure

Short tenors have not shown the same recovery from their sharp put-skew during the selloff as BTC’s have

.jpg)

.jpeg)

.jpg)

.jpg)

.jpg)

.jpg)